Mortgage rates have become one of the most closely watched indicators in the housing sector, shaping consumer sentiment, influencing sales velocity, and affecting builder strategy. While the day-to-day changes can feel unpredictable, the underlying forces are well known and worth watching closely.

Several key economic signals consistently set the tone for mortgage rate direction, and together, they form a roadmap that builders and developers can use to navigate market uncertainty. These key indicators to watch were covered in our latest housing market presentation and are visualized below.

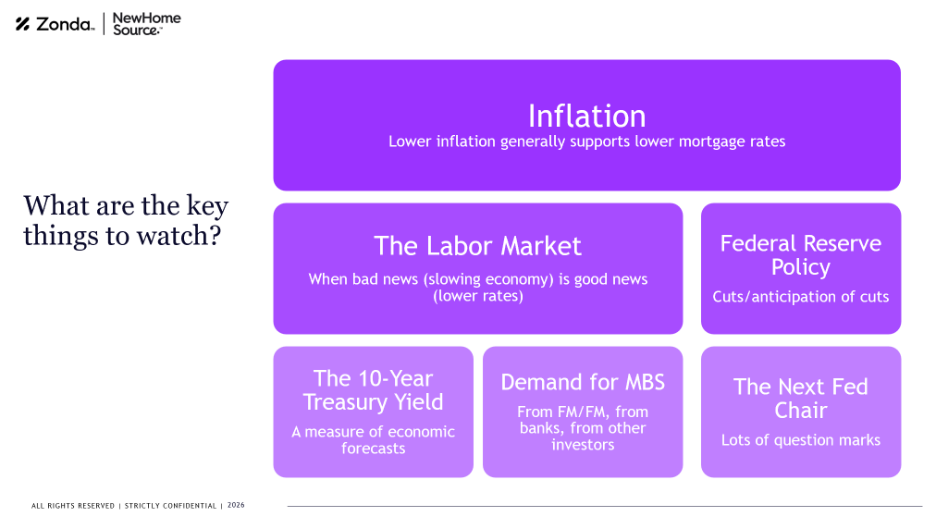

Inflation. At the top of that roadmap is inflation; mortgage rates tend to fall when inflation cools. The past few years have shown that even small improvements in inflation expectations can ripple quickly through financial markets. When inflation moderates, mortgage rates usually follow, offering consumers a bit of affordability relief. Conversely, persistent price increases can hold rates higher for longer, limiting buyers even in otherwise strong markets.

The labor market. Employment trends act as a barometer for overall economic momentum. Softer labor data such as slower job growth or rising unemployment can pull mortgage rates down as bond investors place their money in safe haven assets. In other words, bad news for the economy can, at times, be translated into good news for home shoppers. Builders watching employment indicators can often get an early read on shifts in rate direction, helping them adjust incentives and marketing efforts proactively.

Federal Reserve policy. The Federal Reserve also plays a pivotal role. While the Fed does not set mortgage rates directly, its policy decisions heavily influence them. Rate cuts, or even the anticipation of cuts, generally support lower mortgage rates. Conversely, signals that the Fed may stay restrictive often push borrowing costs higher. With leadership transitions and evolving perspectives inside the central bank, the market may see periods of heightened uncertainty, making Fed communication essential reading for anyone tied to housing.

The next Fed chair. Related, leadership at the Federal Reserve adds an additional layer of uncertainty. A new Fed chair may bring different priorities, communication styles, or economic interpretations, all of which affect market expectations. Even subtle changes in messaging can influence how investors position themselves, ultimately flowing through to the mortgage market.

The 10-year Treasury yield and the demand for mortgage-backed securities. Beyond broad monetary policy, the bond market provides another important clue. The 10-year Treasury yield remains one of the most reliable indicators of where mortgage rates are headed because mortgages are typically packaged and sold to investors who compare their yield to Treasurys. When Treasury yields rise, mortgage rates typically move up in tandem. When they fall, mortgage rates usually soften.

While this isn’t an exhaustive list of what can and does move interest rates, understanding some of the key drivers (i.e. inflation and the labor market) is important. With these indicators in view, housing professionals can better prepare for the shifts ahead and align strategies with evolving economic conditions.

The insights in this article were taken from a Zonda Economics presentation given earlier this year.